English

English Chinese

ChineseScan QRCode

On April 17th, Japanese media outlet "Toyo Keizai Online" reported that Honda had decided to shut down one fuel vehicle factory each at Guangqi Honda and Dongfeng Honda due to sluggish sales in China. Specifically, the factory associated with Guangqi Honda will cease production in June 2026, while the Dongfeng Honda factory will follow suit in 2027. It is understood that the two joint ventures have a total of four fuel vehicle factories in China, and the closure of two of them this time is primarily aimed at addressing overcapacity. Honda's predicament is not unique. Since last year, five joint venture automakers, including Volkswagen, General Motors, and Mitsubishi, have chosen to shut down factories. The once dominant joint venture giants in the Chinese market are collectively undergoing a profound restructuring of production capacity and market reshuffle.

01. The "pain" of joint venture giants

Honda's predicament is the most severe. In terms of sales volume, Honda's sales in China peaked in 2020 (annual sales of 1.62 million units) and have declined for five consecutive years, falling to 645,300 units in 2025 and only 122,000 units in the first quarter of 2026, with no signs of recovery in sight. In terms of production capacity, Honda built two new electric vehicle factories in 2024, with a total production capacity of 1.73 million units. However, due to the sharp decline in sales, the current annual production capacity has dropped to 1.2 million units, including 960,000 fuel vehicles and 240,000 electric vehicles. After the closure of two fuel-powered factories, Honda's production capacity will further shrink to 720,000 units. In 2025, Honda's production in China was only 680,000 units, with an operating rate of about 50%. More critically, Honda plans to start producing electric vehicles under the leadership of GAC and Dongfeng from 2028, with the research and development leadership shifting to its Chinese partners. This has also caused concern among Honda's component suppliers, as after the reduction in production capacity, their business share has plummeted, and profitability may be difficult to maintain. Volkswagen Group also faces considerable pressure. In 2025, Volkswagen's sales in China were 2.9281 million units, down 9.5% year-on-year. Shi Wentao, CEO of Volkswagen's passenger car brand, admitted, "I am well aware that we are actually losing our core." In the first quarter of 2026, Volkswagen delivered only 548,700 units in China, down 14.8% year-on-year, making it the group's largest regional market decline during the same period. The situation with General Motors is slightly different. In 2025, SAIC-GM sold 435,000 units, up 22.99% year-on-year. The official response to the reason for the factory closure is mainly structural capacity optimization: firstly, there is severe overcapacity, with a total production capacity of 2.6 million units across four major bases, but sales in 2024 were only 435,000 units, with a utilization rate of less than 17%; secondly, the fuel-powered factory is located in a remote area, making it difficult to undertake the layout of electric vehicle transformation. After the factory was sold to Geely for renovation, SAIC-GM was able to concentrate resources on its three major bases in Shanghai Jinqiao, Yantai Dongyue, and Wuhan. Overall, the structural pressure faced by joint venture brands in the Chinese market continues to accumulate.

02. There are still three common challenges

In this round of structural adjustment, three common challenges faced by joint venture (JV) automakers have emerged clearly. Firstly, the basic market for fuel-powered vehicles is being eroded by domestic brands. According to data from the China Passenger Car Association, the annual penetration rate of new energy vehicles (NEVs) reached 47.6% in 2024 and 57% in 2025, an increase of nearly 10%. The industry predicts that the NEV penetration rate will rise to around 60% in 2026. Another set of data shows that in 2025, domestic brands' share in both the retail and wholesale markets exceeded 65%. Evidently, against the backdrop of the accelerating shrinkage of the fuel-powered vehicle market, domestic brands, leveraging their first-mover advantage in the NEV sector, are squeezing the living space of JV brands in various market segments. Taking the three major Japanese automakers as an example, their combined sales in China in 2025 amounted to approximately 3.08 million units, accounting for less than 9% of the total Chinese automotive market sales of 34.4 million units. The once solid brand moat of JV brands is rapidly disintegrating. Secondly, the transformation towards electrification is slow, and product competitiveness is insufficient. In March this year, the penetration rate of NEVs among domestic brands reached 73.5%, while mainstream JV brands only accounted for 6.2%. In terms of the retail share of NEVs, domestic brands accounted for 66.6%, while mainstream JV brands accounted for only 3.4%. Some industry experts predict that by 2030, the domestic market penetration rate of NEVs in China will exceed 70%, making it the absolute majority in the market. This also means that JV automakers, which rely on fuel-powered vehicles as their basic market, still need to continue to accelerate their pursuit of NEV penetration. The Volkswagen Group is taking a more aggressive step in catching up. By 2026, Volkswagen will launch 13 NEV models in the Chinese market, covering pure electric, plug-in hybrid, and extended-range products; by 2027, NEV models will account for more than half of the product portfolio; and by 2029, over 30 new NEV models will be launched. Thirdly, the localization of the R&D system lags behind, making it difficult to meet Chinese consumers' demand for intelligence. Multinational automakers have long adopted the strategy of "one model for the whole world", with R&D leadership concentrated in overseas headquarters. The product iteration cycle can last for several years, while domestic brands have compressed model updates to just a few months. Since 2026, GAC Toyota has expanded the coverage of "Chief Engineer in China" and handed over model development decision-making power to local teams. However, such "delegation" actions are still rare in the JV camp, and a large number of JV brands are still in a passive position in the intelligence arms race.

03. Self-rescue amid structural decline of fuel-powered vehicles

While joint venture automakers are under comprehensive pressure, the entire fuel vehicle market is experiencing structural contraction, and luxury brands are not immune to this trend.

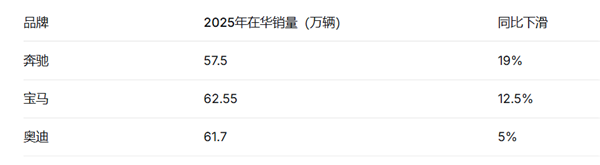

Throughout 2025, the luxury fuel vehicle market experienced a noticeable downward trend. The collective decline of the BBA trio was not a short-term fluctuation, but rather a structural loss amidst the wave of new energy vehicles. Faced with this dilemma, luxury car companies have adjusted their strategies. In June 2025, Konrad Zuse, Chairman and CEO of Mercedes-Benz, announced that the company would adjust its strategic direction and retain internal combustion engine models for a longer period than originally planned. He believed that, given the slower-than-expected adoption of electric vehicles, promoting both fuel and electric vehicles simultaneously was the most rational choice, stating that "neither technology can be abandoned." Audi subsequently made a strategic shift: it announced the cancellation of the comprehensive electrification target set by the previous management for 2033 and no longer set a timeline for discontinuing internal combustion engine production. The core strategy for luxury car companies to maintain their gasoline vehicle business is "integrating intelligence into both gasoline and electric vehicles," injecting intelligent capabilities into fuel vehicles to preserve brand value and market share. FAW Audi has launched the PPC luxury fuel intelligent platform, and the Audi A5L is equipped with Huawei's Qiankun intelligent driving technology, becoming "the world's first fuel vehicle equipped with Huawei's Qiankun intelligent driving system." Given that the gasoline vehicle market still accounts for half of the market share, "integrating intelligence into both gasoline and electric vehicles" has become a key path for luxury car companies to maintain their basic market position. Although the effectiveness remains to be tested, it seems premature to write off fuel vehicles. What is your view on the statement that "the exit of fuel vehicles is only a matter of time"?

AMS2024 Exhibition Guide | Comprehensive Exhibition Guide, Don't Miss the Exciting Events Online and Offline

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号